Proprietary Research

Protean Research Lab

Quantitative frameworks and proprietary models powering Protean's investment process. Interactive visualizations updated as new data becomes available.

Published Research — SSRN Working Paper

Multi-Scale Signal Decomposition for Market-Neutral Equity Strategies

Austin Lazar • Protean Asset Management LLC • May 2026

Ensembling conviction signals across multiple temporal scales produces systematically

superior risk-adjusted returns versus any single-timeframe approach. Applied to a

point-in-time S&P 500 universe over 1,045 trading days with walk-forward validation

showing out-of-sample Sharpe of 3.96 exceeding in-sample Sharpe of 2.11.

2.68

Sharpe Ratio

27.3%

CAGR

−4.1%

Max Drawdown

−0.028

Beta to SPY

Macro — Liquidity Regime

Macro Fractal Complexity

Cross-Asset Liquidity Regime Classification | D(20) Fractal Dimension | 22 Macro Securities | Week Ended May 22, 2026

Macro — Leading Indicator

CPDP Model vs PCE — 16-Month Leading Indicator

CPDP Model (16mo lag) vs PCE CYOY Index | Proprietary Framework | Monthly Data

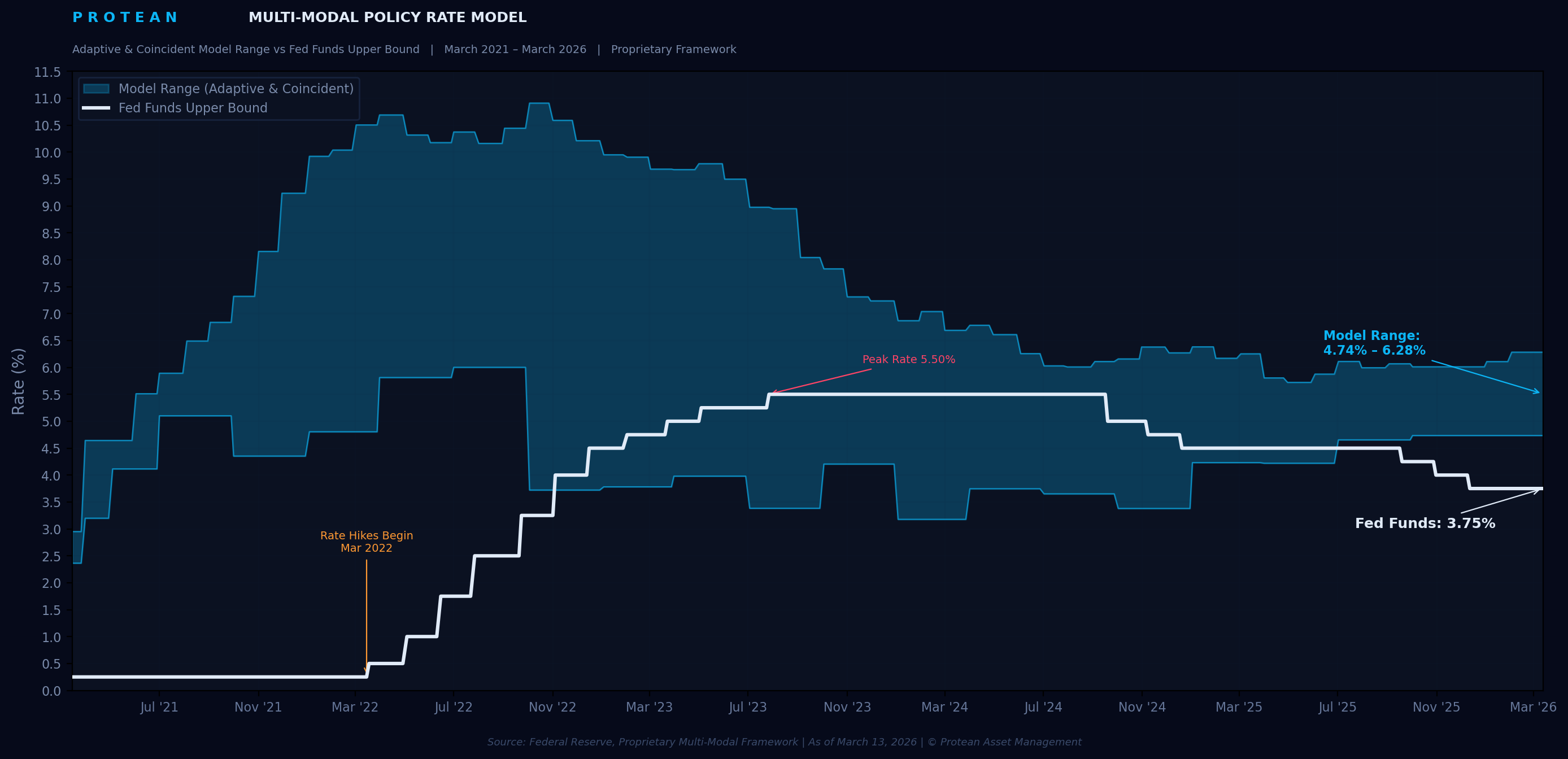

Macro — Policy Rate Framework

Multi-Modal Policy Rate Model

Adaptive & Coincident Model Range vs Fed Funds Upper Bound | Proprietary Framework | March 2021 – March 2026

3.75%

Fed Funds (UB)

4.74 – 6.28%

Model-Implied Range

–0.99%

Gap Below Floor

Microstructure — Dealer Positioning

Dual-Product Dealer Gamma Map — SPX + SPY Unified

Proprietary GEX Framework | Black-Scholes Gamma | Bloomberg OMON Data | As of April 16, 2026 (EoD)

~6,975

Gamma Flip

+$28.2B

Net GEX / 1%

0.27x

Combined PCR

2.04M

OI @ 7,000 Magnet